Birkenstock (BIRK): A 250-Year-Old Brand That Can Say “No” and Still Grow

- Max Teh

- Mar 8

- 10 min read

KEYPOINTS:

🔑 Functional demand over fashion cycles: Birkenstock’s orthopedic footbed design anchors demand in comfort and foot health rather than seasonal fashion trends.

🔑 Durable brand with strong economics: A distinctive product architecture, disciplined distribution strategy, and European manufacturing heritage support pricing power and ~58% gross margins.

🔑 Moderate near-term upside, stronger long-term potential: As of 13 May 2026, the stock trades at ~15× P/E the stock appears fairly valued (~18% modeled CAGR for the next 3 years), but longer-term returns could improve if consumer spending strengthens and valuation multiples expand.

Table of contents

Disclaimer: This communication is provided for information purposes only and is not intended as a recommendation or a solicitation to buy, sell or hold any investment product. Readers are solely responsible for their own investment decisions.

Introduction

Birkenstock is one of the rare consumer brands whose demand originates from functional necessity rather than fashion cycles.

While most footwear companies compete primarily on seasonal designs or marketing trends, Birkenstock’s demand is rooted in something far simpler:

foot comfort and health.

Over time, this functional foundation has gradually evolved into cultural relevance. The result is a brand that sits at the intersection of orthopedic credibility and lifestyle acceptance.

This combination gives Birkenstock a competitive positioning that few footwear brands possess, allowing the company to maintain pricing power while steadily expanding its global footprint.

Birkenstock's Brand Power: The Ability to Say “No” and Still Grow

One of the clearest indicators of brand strength is the ability to reject opportunities that could dilute long-term brand value.

Birkenstock has demonstrated this discipline multiple times.

In 2018, management rejected collaboration proposals from Supreme, despite the brand’s long track record of successful partnerships. Management believed that collaborations driven purely by fashion hype would dilute Birkenstock’s core identity.

Even more telling was the company’s decision in 2016 to exit Amazon entirely due to counterfeiting issues and loss of brand control.

Instead of hurting sales, the opposite happened.

Consumers followed the brand.

Website traffic increased dramatically — growing roughly 10× after the Amazon exit — reinforcing the idea that Birkenstock possesses genuine brand pull rather than platform dependence.

This distinction matters.

It means Birkenstock controls its distribution rather than relying on third-party platforms to generate demand.

A 250-Year-Old Brand That Was Never Built for Scale

At first glance, Birkenstock’s relatively modest revenue base for a company founded in 1774 might seem surprising.

In reality, this reflects intentional restraint.

For most of its history, Birkenstock was a family-owned shoemaking business operating primarily in Europe, focused on craftsmanship rather than global scale.

The company behaved more like a specialized craft manufacturer than a global consumer brand.

This began to change in 2021, when private equity firm L Catterton (backed by LVMH’s Arnault family) acquired a majority stake.

Rather than reinventing the brand, the new ownership focused on:

• professionalizing management

• expanding manufacturing capacity

• scaling global distribution

The 2023 IPO was therefore less about funding growth and more about normalizing the balance sheet following the leveraged buyout.

Structural Demand Tailwinds: Comfort Over Cycles

One of the most underappreciated drivers behind Birkenstock’s growth is the structural increase in consumer awareness around foot health.

Conditions such as:

• plantar fasciitis

• flat feet

• chronic foot fatigue

are increasingly discussed by consumers and healthcare professionals.

Search data for terms like “supportive shoes” and “plantar fasciitis footwear” has steadily increased over the past decade.

![Global plantar fasciitis treatment market is projected to grow from USD 1.28 billion in 2024 to USD 3.45 billion by 2033, expanding at a CAGR of 11.9% [source: Grand View Research]](https://static.wixstatic.com/media/07074b_d06153b0a1874ba3852e1cce10ae8828~mv2.png/v1/fill/w_980,h_551,al_c,q_90,usm_0.66_1.00_0.01,enc_avif,quality_auto/07074b_d06153b0a1874ba3852e1cce10ae8828~mv2.png)

While Birkenstock is not a medical device company, its cork-latex footbed design naturally aligns with these comfort-seeking behaviors.

This gives the brand a defensive demand base that is less dependent on fashion cycles.

Product DNA: A Design That Never Needed Reinvention

The defining feature of Birkenstock footwear is its cork-latex footbed, designed to distribute body weight evenly across the foot.

What makes the product remarkable is not constant redesign.

It is consistency.

The Birkenstock footbed has remained fundamentally unchanged for decades — refined rather than reinvented.

This stability gives the product a timeless quality, allowing it to transcend fashion cycles.

Celebrity adoption further reinforced this cultural normalization.

Perhaps the most famous example is Steve Jobs, who wore Birkenstocks for decades. In 2022, his worn pair sold at auction for over $220,000, the highest price ever paid for sandals.

Competitive Positioning: Owning the Intersection

Birkenstock occupies a very specific niche within the footwear industry:

Footwear that is both orthopaedic and socially acceptable as everyday wear.

Most competitors sit on only one side of this spectrum.

Category | Typical Brands |

Orthopedic footwear | Vionic, Vivobarefoot |

Performance footwear | Nike, Adidas |

Fashion footwear | Luxury brands |

Birkenstock sits directly in the middle — combining:

• functional foot support

• heritage manufacturing

• lifestyle acceptance

Even closer competitors such as ECCO lack Birkenstock’s historical brand equity and cultural relevance.

This positioning reduces the risk of rapid displacement by trend-driven competitors.

Another factor supporting Birkenstock’s brand credibility is its manufacturing footprint. A large portion of its core products are still produced in Germany and assembled in Portugal, reinforcing the brand’s heritage as an orthopedic footwear specialist.

For consumers prioritizing foot health and product quality, European manufacturing can serve as an additional signal of craftsmanship and reliability, particularly compared with competitors that rely primarily on outsourced production in Asia.

This distinction becomes more evident in how competition plays out within the category. Lower-priced substitutes may replicate the appearance, but they struggle to replicate the post-purchase experience, particularly in durability, consistency, and long-term comfort.

Over time, this creates a separation between trial and repeat behavior, where consumers who enter through substitutes often migrate back to the original. In this dynamic, knockoffs tend to expand awareness of the silhouette, but reinforce the positioning of the incumbent rather than displacing it.

Financial Profile (Latest LTM – Dec 2025)

Interestingly, Birkenstock’s business model shares similarities with companies such as Crocs, where a single core product architecture drives the majority of sales. Both brands have built strong pricing power around a distinctive and recognisable design rather than relying on constant technological innovation.

Company | Gross Margin |

Birkenstock | ~58% |

Crocs | ~58% |

Nike | ~41% |

Skechers | ~52% |

Birkenstock operates with margins closer to premium consumer brands than typical footwear companies.

Latest LTM financials (Dec-2025):

Metric | Value |

Revenue | €2.14B |

Gross Margin | ~58% |

Operating Margin | ~26% |

Net Income | €379M |

EPS | €2.03 |

Free Cash Flow | €268M |

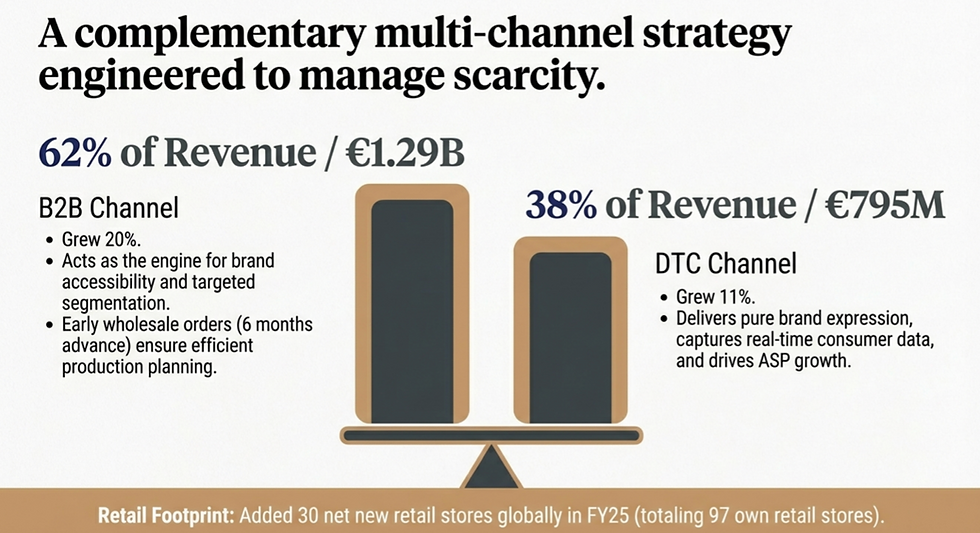

Revenue has grown consistently over the past few years, reaching €2.1B in FY2025, representing roughly 16% YoY growth. (StockAnalysis)

Margins remain unusually strong for the footwear industry:

• Gross margin ~58%

• Operating margin ~26%

• Net margin ~17%

These margins are supported by three structural advantages:

strong pricing power

direct-to-consumer expansion

engineered distribution that limits over-supply

Growth Drivers

Birkenstock’s growth strategy focuses on three main areas.

1. Retail Expansion

The company plans to open ~40 new company-owned stores in FY2026, expanding its direct retail presence globally.

Direct-to-consumer sales capture the full retail margin and therefore tend to be margin-accretive over time.

2. Geographic Expansion

Asia-Pacific remains significantly underpenetrated and represents a major long-term growth opportunity.

That said, investors should monitor closely on the Climate and Production Maintenance Friction Birkenstock could face in their APAC expansion plan.

3. Product Expansion

Closed-toe footwear (such as the Boston clogs) and professional footwear categories are growing faster than traditional sandals and now represent an increasing share of revenue.

Risks to Monitor

Despite the strength of the brand, several risks should be monitored.

Tariffs

Recent trade tensions and import tariffs could impact margins.

Management has indicated that tariffs could reduce gross margins by roughly ~100 basis points in FY2026. (Reuters)

Retail Expansion Costs

The company’s aggressive store expansion strategy may temporarily increase:

• SG&A expenses

• operating leverage risks

• execution challenges in new markets

Economic Sensitivity

Although Birkenstock benefits from comfort-driven demand, its premium price positioning means that sales could still be affected during periods of consumer spending slowdown.

i. Climate and Product Maintenance Friction in APAC Markets

While the APAC region represents one of Birkenstock’s most important long-term growth opportunities, investors should also be aware of potential structural frictions unique to the region.

The company has reported ~36% CAGR growth in APAC over the past two years, yet the region still accounts for only ~11% of total revenue, leaving substantial room for expansion. This underpenetration is precisely why management has positioned APAC as a key future growth engine.

However, there are several factors that could make scaling adoption in the region somewhat more complex compared with Europe and the Americas.

First, many APAC markets have significantly more humid climates and higher rainfall levels, particularly in Southeast Asia and parts of East Asia. Birkenstock’s core products rely on natural materials such as cork, latex, and leather, which can be more sensitive to prolonged exposure to moisture, sweat, and tropical conditions.

Users in these climates often report that the footbeds develop darker or oilier surfaces more quickly, largely due to higher humidity and perspiration levels.

In addition, tropical conditions may accelerate wear on the cork-latex construction, potentially leading to shorter product lifespans compared with usage in cooler or drier regions.

Second, repair infrastructure in APAC is currently less developed than in Europe, where Birkenstock has a long history and established cobbler networks capable of repairing cork soles and footbeds. In markets where repair services are less accessible, consumers may rely more heavily on replacement purchases rather than refurbishment.

Finally, product maintenance and the break-in period may also present minor adoption friction for first-time users. Birkenstock’s cork footbeds typically require several weeks of wear to mold comfortably to the user’s feet, and cleaning the footbed can require more care compared with fully synthetic footwear.

These factors may not prevent Birkenstock from expanding successfully in APAC, but they do highlight the importance of localization strategies, such as:

expanding repair networks

educating consumers on product care

promoting more climate-appropriate models (e.g., EVA or leather-lined footbeds)

adapting distribution and after-sales support

As APAC expansion is still relatively early, investors should continue monitoring customer satisfaction, repeat purchase behaviour, and brand perception in the region.

If product durability or maintenance expectations diverge meaningfully from consumer expectations, this could eventually slow adoption or weaken word-of-mouth growth in these markets.

Portfolio Perspective: An AI Hedge

One interesting aspect of Birkenstock is that it can serve as a portfolio hedge against expensive technology and AI-related stocks.

During periods when technology valuations expand significantly, investors often search for businesses with:

• strong pricing power

• durable brands

• predictable demand

Birkenstock fits this profile.

Its business model is largely independent of technological cycles and instead tied to consumer lifestyle and comfort demand.

However, the brand still sits in a premium price bracket, typically selling footwear in the $150–$300 range.

Because Birkenstock targets a broader population than ultra-luxury brands, demand could still soften during economic downturns if consumers reduce discretionary spending.

As a result, while Birkenstock can act as a defensive consumer brand, it is not entirely immune to macroeconomic cycles.

Valuation Perspective

At around $34 per share as of 13 May 2026, Birkenstock trades at approximately:

~15× P/E

~12× EV/EBIT

This valuation appears broadly reasonable for a business with double-digit revenue growth, strong margins, and a durable global brand.

Based on my forward model, however, the expected return over the next three years is roughly ~18% CAGR under relatively conservative assumptions.

In constructing the model, I intentionally applied slightly conservative inputs across

tapering of revenue growth (~11% CAGR until 2028),

compressing margin trajectory (decrease of GPM% to 57% from 59% and OPM% to 23% from 26%),

and conservative share count (assuming no buybacks, although management mentioned ~200m buyback program).

🔗 refer to full model here.

The objective is to increase the probability of being directionally correct from a probabilistic and mathematical standpoint, rather than relying on optimistic assumptions that may not materialize.

Under these assumptions, meaningful upside over the next few years would likely require moderate multiple expansion, for example from roughly ~15× to ~20× earnings.

As such, the near-term return profile appears reasonable but not particularly compelling, especially relative to higher-growth sectors such as technology.

Longer-Term Return Potential

Over a longer horizon (for example five to ten years), Birkenstock’s returns could exceed the modeled projections if several conditions become more favorable.

First, stronger economic conditions could support higher discretionary spending, which would benefit premium consumer brands.

Second, improved equity market sentiment could allow valuation to expand toward higher levels. For instance, if the stock were valued closer to ~24× earnings, which would still imply a reasonable PEG ratio — returns could approach ~25% CAGR.

Third, reduced geopolitical tensions and tariff pressures could support margins by lowering supply chain costs.

Taken together, while Birkenstock’s near-term upside appears moderate, the company still possesses the characteristics of a durable consumer brand capable of steady long-term compounding.

Market Behaviour Since IPO

Since its IPO in late 2023, Birkenstock’s share price has experienced periods of meaningful volatility and has largely traded sideways overall.

In the early months following the listing, the stock often traded at premium valuation levels, reflecting strong investor enthusiasm for the brand’s growth potential. Over time, however, valuation multiples have gradually normalized as the market reassessed the company’s growth trajectory.

At the current price level, Birkenstock appears closer to fair value — and potentially slightly oversold relative to its historical trading range.

That said, the stock may continue to experience elevated volatility in the near term. As a relatively recent IPO, the market is still in the process of forming a stable long-term valuation framework for the company.

As a result, investors should be prepared for continued price fluctuations while the stock undergoes this valuation adjustment phase.

For investors interested in the company’s long-term prospects, Birkenstock may therefore be better approached with a multi-year investment horizon (five years or longer) rather than a short-term trading mindset.

Investment Perspective

Birkenstock is not a hyper-growth company.

What it offers instead is something arguably rarer:

a durable consumer brand capable of compounding steadily over long periods of time.

Its key strengths include:

• over 250 years of brand heritage

• strong pricing power

• high margins relative to peers

• structural demand driven by comfort and foot health

• backing from LVMH-linked investors

For long-term investors, Birkenstock can serve as:

• a steady compounder

• a portfolio stabilizer during tech-heavy cycles

• a consumer brand with defensive characteristics

provided it is acquired at a reasonable valuation.

Comments